Summary

In the past year, the Mega Millions and Powerball

lottery jackpots have shattered records, rocketing

past half a billion dollars each.

Should you have

bought a ticket? Would any size jackpot make

a ticket an economically rational investment?

Mega Millions

and

Powerball

are a popular multi-state lotteries in the United States

that use what's called a "progressive jackpot."

If no one wins the jackpot in a lottery drawing,

the prize money is carried

forward into the next drawing's prize pool, combined with new

money from the previous drawing's sales.

Most people know that lotteries are losing propositions

under normal conditions, but

progressive jackpots can, in theory, grow without bound.

Since the probability of winning a jackpot remains fixed,

an intriguing possibility emerges:

might it actually become profitable, in

expectation,

to buy a lottery ticket?

Many people have already observed that

a lottery ticket purchased in isolation will

have a positive expected value

if the post-tax jackpot grows larger than the

odds of winning.

However, larger jackpots generate higher ticket sales,

and in the case of a tie the jackpot is split among all winners.

Some

analyses

account for the effect of ties, but none that I've found

have observed that as the jackpot grows,

ticket sales appear to increase super-linearly.

This means there is a point of diminishing return

where the negative expectation due to ties

outweighs the positive expectation due to having a larger jackpot.

Taking this into account,

it is unlikely that buying a lottery ticket is

ever profitable in expectation,

no matter how big the jackpot gets.

Winning If You're the Only Player

Let's start with the simplest case.

Imagine that you are the only person buying a

Mega Millions ticket.

A ticket costs $1, and

the probability of winning the jackpot is

1

in 175,711,536.

Therefore, if the jackpot is expected to yield exactly

$175,711,536, then your $1 ticket has an expected value of

$1 -- it's an even-money proposition, albeit one with very

high variance.

To simplify the calculations, assume for now that the

jackpot is the only prize; we'll consider the relatively

small effect of the smaller prizes in a moment.

I'm also assuming there are no intangible benefits to playing, such

as the thrill you get from watching the draw.

And keep in mind just how low the probability of winning is:

imagine someone has laid down a strip of pennies along the

2,000 miles (3,200 km) of highway

from Los Angeles to Chicago, and put a secret "X" on

just one of them. Take a road trip, stop randomly

on the side of the road, and pick up a single penny.

You are about as likely to find the "X"

as you are to win the Mega Millions jackpot.

But this is no time for such negative thinking!

It might seem at first glance that any time the jackpot

grows beyond $175.7 million, it's economically

rational to buy a ticket. Buying a ticket for March's

$640 million drawing would have been a smart move, right?

Slow down, big dreamer.

Unfortunately, an advertised jackpot of $175.7 million

doesn't actually yield $175.7 million in prize money. There

are two important deductions to take into account:

- Net present value. The advertised jackpot is

what Mega Millions will pay you in 26 yearly installments.

However, the dollar you use to buy your ticket is an

up-front cost today. For

the comparison to be valid, we have to use the net present

value of the jackpot -- that is, the immediate one-time cash

payout option. (Equivalently, we could consider the cost

of the ticket to be $1 invested for 26 years.)

Mega Millions pays cash up-front at 63% of the

advertised jackpot value.

- Taxes. The top marginal federal tax

rate is 35%. Not all states have an

income tax -- my home state of Washington does not, for

example -- but

states that do have an average tax rate of about

6%. Between the two, you keep about 59% of your

winnings, depending on your state.

So the world-record

$640

million jackpot in March of 2012 wasn't actually worth

$640 million after all.

Taking tax and present value into account, it was really

"only" worth $640 x 0.63 x 0.59 = $238 million if you'd

been the only person

playing.

That's still a lot -- and it would make the expected value

of a ticket $1.35. Seems like a smart bet so far!

Let's also consider the

other, non-jackpot prizes. They are paid immediately

(without the 26-year annuity), so we only need to

discount them for taxes, not present value.

Multiplying each prize by the probability of winning

it

yields its contribution to the expected

value of a ticket:

| Prize |

Post-Tax Prize |

Odds of

Winning |

Post-Tax

Expected Value |

| $250,000 |

$147,500. |

1:3,904,701 |

$0.0378 |

| $10,000 |

$5,900. |

1:689,065 |

$0.0086 |

| $150 |

$88.5 |

1:15,313 |

$0.0058 |

| $150 |

$88.5 |

1:13,781 |

$0.0064 |

| $7 |

$4.13 |

1:306 |

$0.0135 |

| $10 |

$5.9 |

1:844 |

$0.007 |

| $3 |

$1.77 |

1:141 |

$0.0126 |

| $2 |

$1.18 |

1:75 |

$0.0157 |

| Total |

|

|

$0.107 |

The non-jackpot prizes add a total of 10.7 cents of

expected value to a ticket, independent of the jackpot

size.

Added to the $1.35 of expected value from the

jackpot,

a ticket for a $640 million jackpot

purchased in isolation

would be worth

an expected $1.46 -- more than its cost of $1!

Were those people

standing

in line for two hours to buy tickets doing so

for good reason?

Wait a second. I keep saying a ticket would be worth

$1.46 when purchased "in isolation," but all those

people in line were buying tickets, too.

What if you're not the only person playing?

The problem of ties

The analysis so far assumes you're the only one buying

a ticket. The problem is that you aren't.

If more than one ticket hits the jackpot, the prize is split

equally among all the winners, reducing its value to each

winner.

To make the problem concrete, let's look at the

$640 million jackpot in 2012 again.

According to

LottoReport.com,

a site that has recorded the sales figures for every Mega Millions

drawing since 2007,

there were nearly 652 million tickets sold to

hopeful future private jet owners.

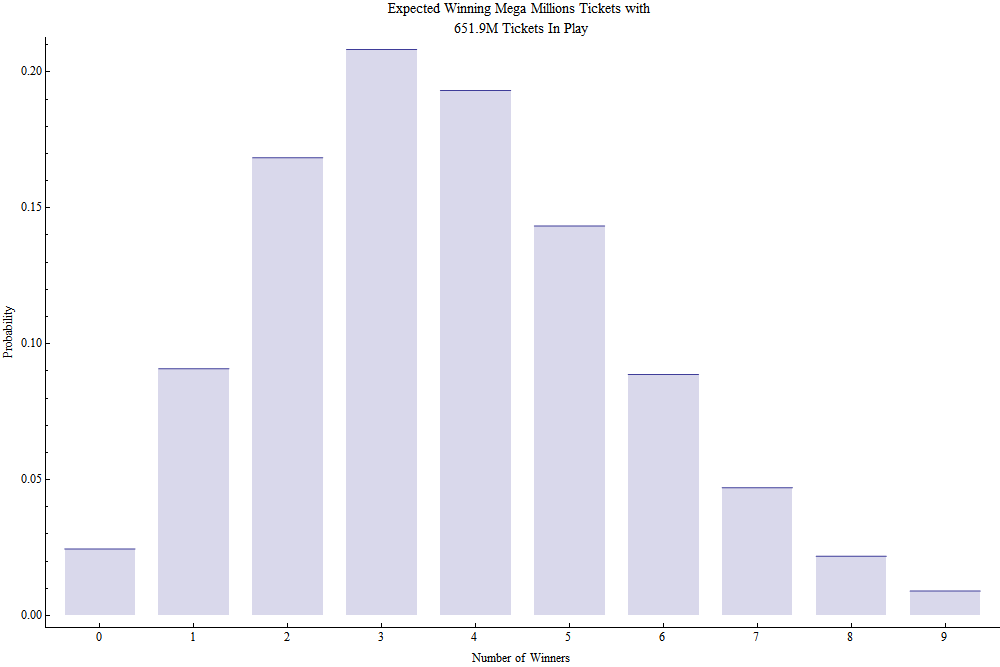

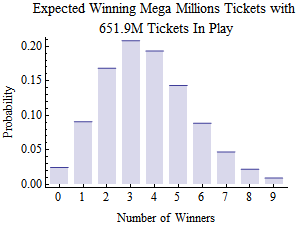

Let's call this n.

Each ticket was independent and had a 1 in 175.7 million

chance of winning. Let's call this p. The

Poisson

distribution with λ = np = 3.71 tells us

how many winners we could expect in that drawing;

it's shown in the plot on the right

(click to enlarge).

To make the problem concrete, let's look at the

$640 million jackpot in 2012 again.

According to

LottoReport.com,

a site that has recorded the sales figures for every Mega Millions

drawing since 2007,

there were nearly 652 million tickets sold to

hopeful future private jet owners.

Let's call this n.

Each ticket was independent and had a 1 in 175.7 million

chance of winning. Let's call this p. The

Poisson

distribution with λ = np = 3.71 tells us

how many winners we could expect in that drawing;

it's shown in the plot on the right

(click to enlarge).

There was a slim 9% chance that a single winner would

keep the entire jackpot, an 88.5% chance that

there would be a tie among two or more winners,

and a 2.4% chance that the jackpot would remain

unclaimed and grow still larger.

The two most likely outcomes were a three-way tie (20.8%)

and a four-way tie (19.3%). (The actual result: a

three-way tie.)

The overwhelming likelihood of a tie had a devastating effect

on the expected value of a ticket.

The most straightforward way to compute the jackpot's

contribution to each ticket's expected value,

suggested by Mark Eichenlaub,

is to divide the expected total payout by the number of

tickets in play.

The expected payout is just the jackpot size

multiplied by the probability that at least one ticket

would win -- 0.975, in this case. Accounting for those

pesky taxes and net present value, the jackpot only

contributed a paltry 35.6 cents to the value of a ticket in

that drawing!

Using some fancier math,

we can dig a little further into why having so many tickets

in play pushes down the expected value of each one.

Let's assume you'd been holding a winning

ticket. There was only

a 2.4% chance that not a single one of the other

652 million tickets out there won, too. We can repeat

this analysis for every realistic number of winners:

compute the

probability of that kind of tie occurring, calculate the

value of the jackpot per winner in that case, and multiply

those two numbers together to get that scenario's

contribution to the expected jackpot. Add them all up,

and we have the expected value of the jackpot, taking ties

into account, as shown in the table below:

Winners

(Including You) |

Probability |

Jackpot Share

($millions) |

Jackpot Share

Post-Tax NPV |

Contribution to

Expected Jackpot

($millions) |

| 1 |

0.0244739 |

640. |

237.89 |

5.82 |

| 2 |

0.0908017 |

320. |

118.94 |

10.8 |

| 3 |

0.168444 |

213.33 |

79.3 |

13.36 |

| 4 |

0.208317 |

160. |

59.47 |

12.39 |

| 5 |

0.193222 |

128. |

47.58 |

9.19 |

| 6 |

0.143377 |

106.67 |

39.65 |

5.68 |

| 7 |

0.0886581 |

91.43 |

33.98 |

3.01 |

| 8 |

0.0469907 |

80. |

29.74 |

1.4 |

| 9 |

0.0217928 |

71.11 |

26.43 |

0.58 |

| 10 |

0.00898383 |

64. |

23.79 |

0.21 |

| 11 |

0.00333314 |

58.18 |

21.63 |

0.07 |

| 12 |

0.00112422 |

53.33 |

19.82 |

0.02 |

| Total |

|

|

|

62.55 |

With

652 million tickets in play,

a 1 in 175.7 million chance of each ticket winning,

a 63% net-present value,

a 41% tax burden,

and an equal split among multiple winners,

the expected value of a $640 million jackpot to a winner

is just $62.55 million, making

the jackpot's contribution to the

expected value of a ticket only 35.6 cents.

Adding back the 10.7 cents of expected value from the non-jackpot prizes,

the total expected value of a ticket in that drawing

drawing

was just

46.3 cents!

This is far worse than the $1.46 we computed

when we ignored the possibility of a tie.

The expected value of a ticket was actually far below its $1

cost. It wasn't such a smart buy after all.

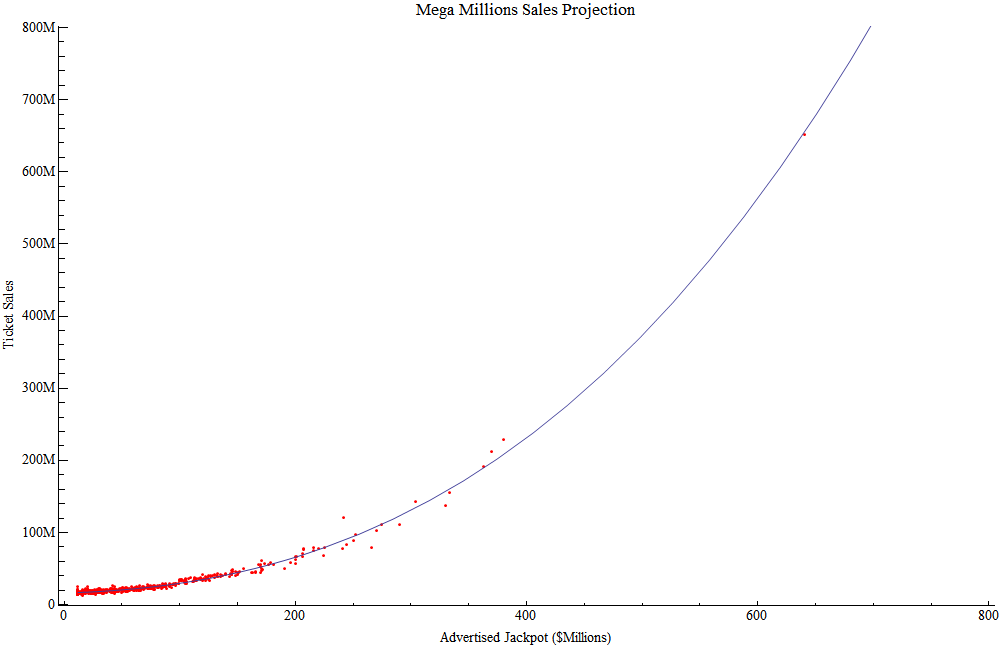

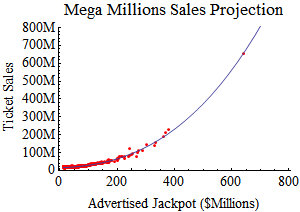

Ticket sales as a function of jackpot size

Unfortunately, we are still not done dumping cold water on

the dreams of lottery winners. (It's a cruel hobby, I

know.) The analysis above took ties into account, but

assumed a fixed number of tickets in play -- 652 million,

to be exact. However, as the media delights in

reporting,

large jackpots incite a

ticket

buying

frenzy, and that makes ties increasingly likely.

Might the increased possibility of a tie

actually make larger jackpots less valuable to the winners?

The first step in answering that question

is to model how the size of the jackpot

will end up affecting the number of tickets that are

bought to try to win it.

Let's return to the excellent data curated by

LottoReport.com.

The red points in the graph on the right

(click to enlarge) are ticket sales

for 618 MegaMillions drawings since 2007, plotted against

the drawing's advertised jackpot.

The lonely point way out at the top right is

the record-breaking March 2012 jackpot of $640 million,

selling 652 million tickets.

The blue line is the best-fit third degree polynomial.

The first step in answering that question

is to model how the size of the jackpot

will end up affecting the number of tickets that are

bought to try to win it.

Let's return to the excellent data curated by

LottoReport.com.

The red points in the graph on the right

(click to enlarge) are ticket sales

for 618 MegaMillions drawings since 2007, plotted against

the drawing's advertised jackpot.

The lonely point way out at the top right is

the record-breaking March 2012 jackpot of $640 million,

selling 652 million tickets.

The blue line is the best-fit third degree polynomial.

As you can see, with jackpots over about $250 million,

ticket sales really start to take off.

However, it's also important to acknowledge that the data

for jackpots above $350 million is sparse, and

non-existent above $640 million.

The curve may not be predictive for unprecedented

jackpots.

If we ever see a

mind-boggling billion-dollar jackpot,

for example,

it predicts frenzied buyers will pay for

a staggering two billion

tickets.

But there's no way to know with certainty what

would actually

happen if a MegaMillions

jackpot grew to such proportions.

Mass hysteria?

The projected sales curve above also paints a grim picture for anyone still

holding out hope that a lottery ticket can ever be an

economically rational investment.

As the jackpot grows in

value,

the number of people who try to win it grows

super-linearly.

This human behavior has a mathematical consequence:

even though the

jackpot itself can theoretically grow without bound, there is

a point at which the consequent ticket-buying

grows to such a fever pitch that the expected value of the jackpot

actually starts going down again.

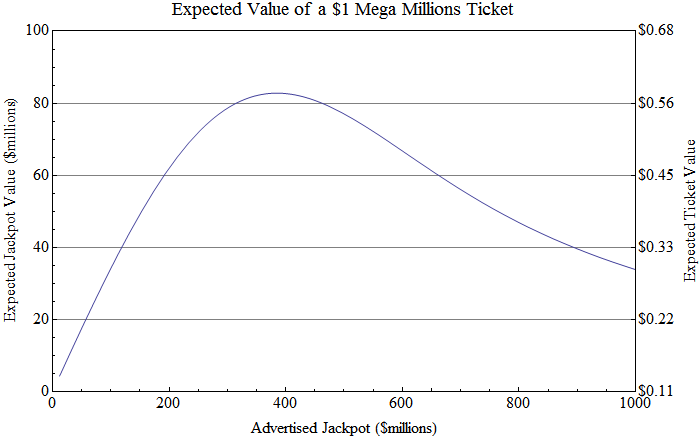

The graph below shows the effect, plotting

advertised jackpot size against expected jackpot value

if you win. It takes everything into account we've

discussed so far: net present value (63% of jackpot), taxes

(41% off), and the increasingly

devastating effect of ties as the number

of tickets grows super-linearly with jackpot size.

The right-hand axis in the above plot shows the expected

value of a ticket at each advertised jackpot size; it is

the expected jackpot value times the 1/175.7 million

probability of winning the jackpot,

plus the 10.7 cents of expected

value

that comes from the non-jackpot prizes.

It peaks at

57.8 cents

when the advertised jackpot reaches $385 million.

The $640 million jackpot in March was already on the

downward part of the curve;

a ticket for that drawing was actually

worth less, in expectation, than a ticket for the

$363 million jackpot that preceded it!

As long as the superlinear ticket growth holds up,

tickets for even bigger jackpots will be worth even less.

In no case does

the expected value of a ticket ever exceed the break-even point of $1.

Thus, Mega

Millions tickets are never an economically rational investment, no

matter how big the jackpot grows.

Powerball

Powerball

is similar to Mega Millions: a multi-state lottery

with a progressive

jackpot that is split equally among winning tickets.

For most of its history, tickets cost $1.

However,

they've made various rules changes since 2012, including

raising

the price of a ticket to $2

and making tickets more likely to win small prizes and

less likely to win the jackpot.

(The Powerball jackpot odds

are now

one in 292 million, much lower than its

former value, nearly identical to MegaMillions, of 1 in 175 million.)

This was clever: selling half as many tickets at twice the

price might seem to be revenue-neutral, but fewer tickets

and lower odds of hitting the jackpot means fewer jackpot

winners.

Fewer jackpot winners makes

larger jackpots more likely, and large jackpots produce

huge spikes in ticket sales.

This effect is important to our analysis because fewer tickets

in play also means fewer ties and more money, in

expectation, for a winner.

Might Powerball

hold the key to financial salvation?

Unfortunately for those of you hoping to buy a sports team,

Powerball turns out to be a bad bet, too.

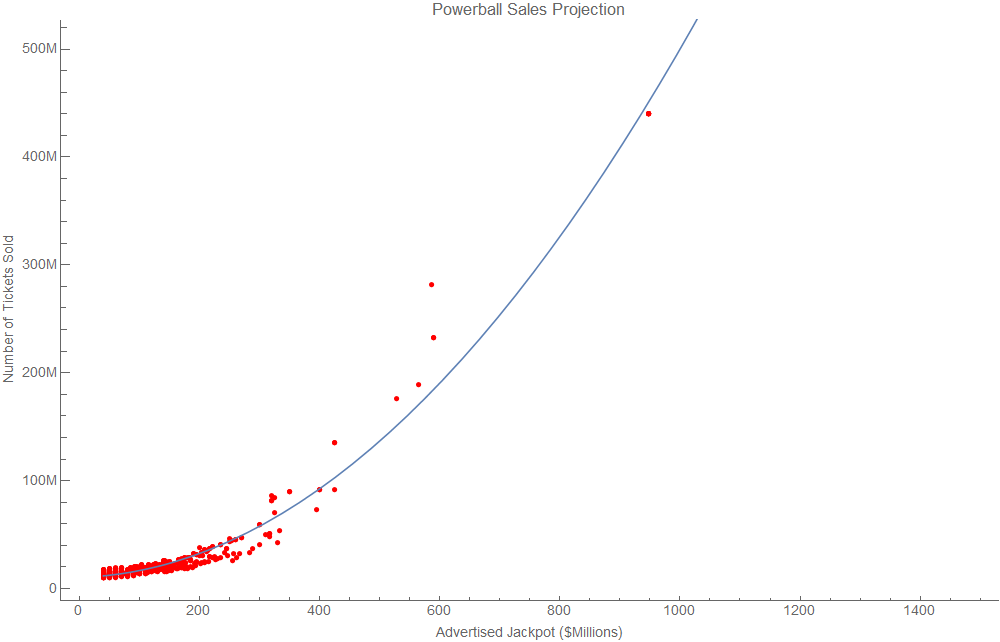

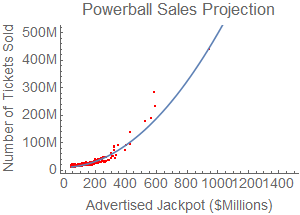

As with Mega Millions, Powerball's ticket sales

(again, from

LottoReport) are

superlinear, shown in the graph on the right

(click to

enlarge).

Included are sales data between the ticket price increase

(January 2012)

and now (January 2016).

The point way out on the top right is the record-breaking

$948 million jackpot on January 9, 2016, that sold

440 million tickets. That point has been given additional

weight in the curve to help better project the behavior with

large jackpots.

Due largely to the $2 tickets producing fewer ticket

sales,

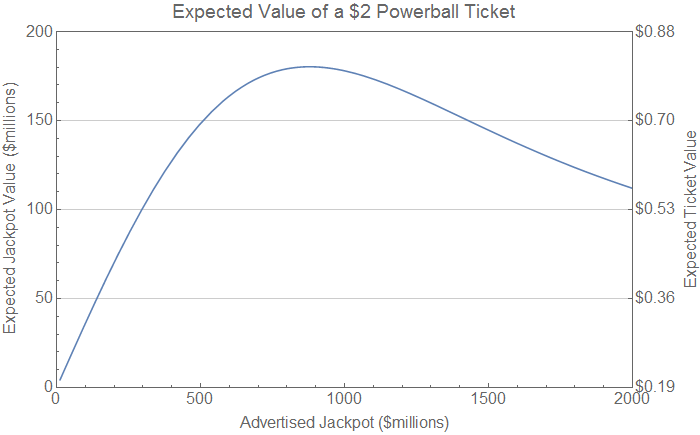

the effect of ties is delayed compared to Mega Millions.

For Powerball, the best ticket value is for jackpots

advertised at about $890 million. We'd expect to

see about 390 million tickets in play, for which

there'd be a 26% chance of no winner,

a 35% chance of a single winner,

and a 39% chance of a tie among two or more winners.

The expected

value of the jackpot to a winner, accounting for ties,

and discounting for taxes and net present value, would

be

$180 million.

Adding in

the expected

value of non-jackpot prizes of

19.1 cents, this gives the ticket an overall expected

value of 80.8 cents -- less than half of its $2

cost. A good deal for state governments'

ailing tax coffers, perhaps,

but certainly not one for players.

Can the models really predict the future?

It's easy to predict how many tickets will be sold for

a drawing when the jackpot is less than a few hundred million

dollars. We have plenty of data for those drawings

showing consistent sales, so interpolation works well.

But how confident can we be in the model when it

extrapolates to jackpots larger than our past experience?

We've had two opportunities to evaluate the sales model's

extrapolation performance

since I first wrote this article in

January of 2011.

At the time, the record for the largest

MegaMillions

jackpot was $380 million.

The following year, in March of 2012, the jackpot grew to

an unprecedented

$640

million.

Ticket sales skyrocketed due in part to intense media coverage,

some of which even described my analysis of why tickets

were still expected to be unprofitable:

The Wall Street Journal's

blog

and

print

editions,

the Washington Post,

the Atlantic,

and Time

Magazine.

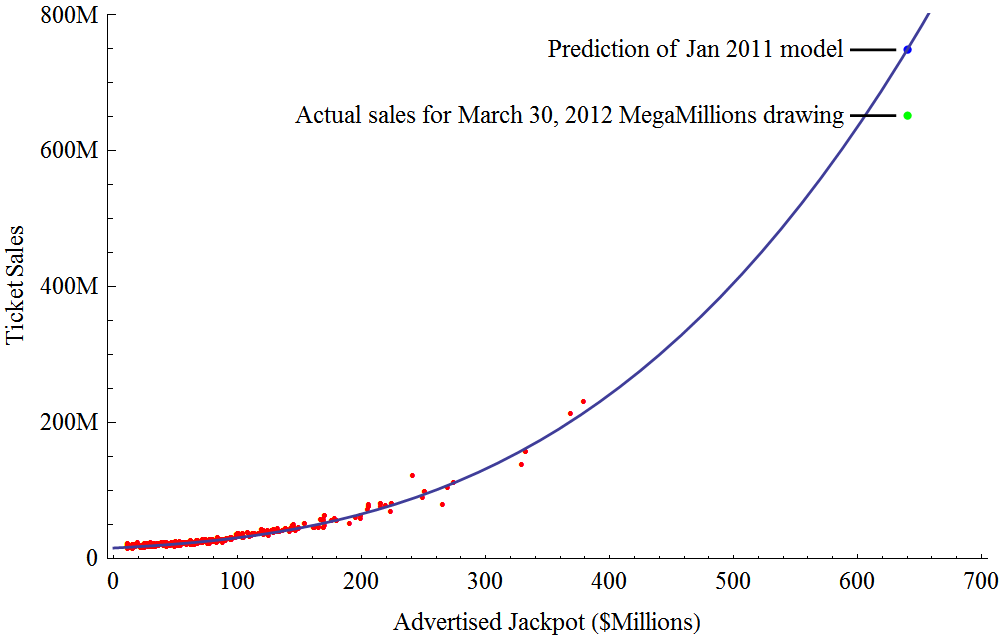

The 2011 model predicted

a Mega Millions jackpot that size would produce

$748m in ticket sales. According

to LottoReport,

actual

sales were $652m, an error of only about 15%.

Based on the drawing's actual ticket sales,

the expected value of a ticket was 46 cents;

the model predicted 42 cents. (10.7 cents of EV came

from non-jackpot prizes in both cases.)

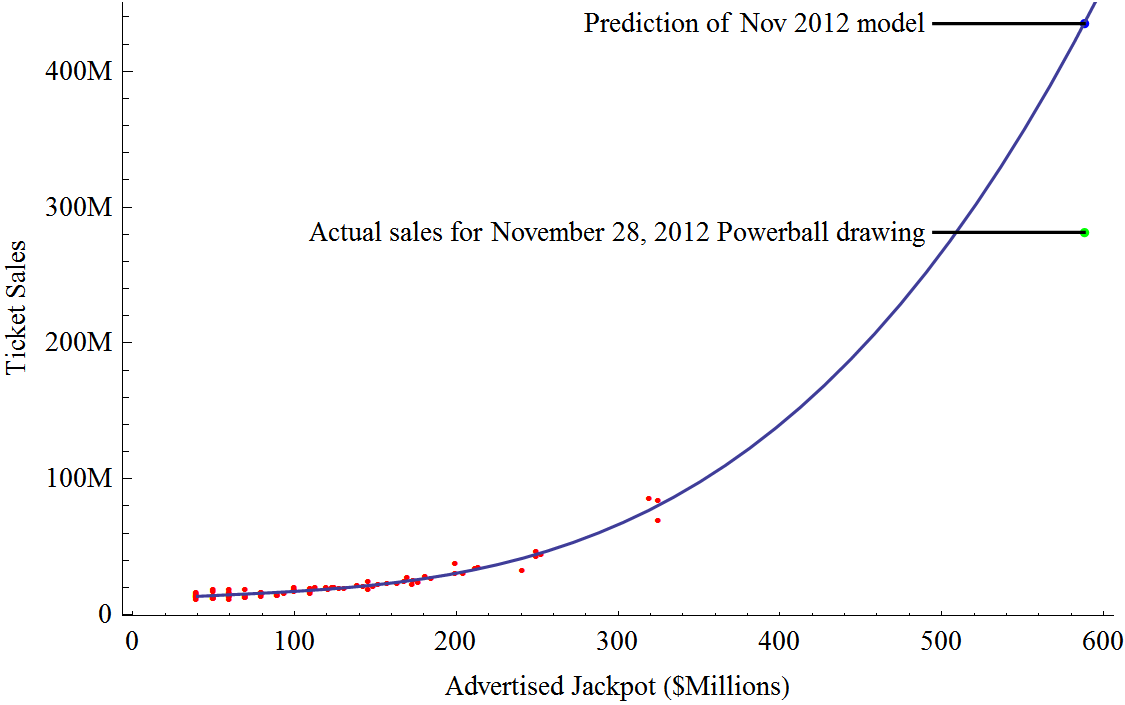

Another test came in November of 2012 when the Powerball

jackpot grew to a record

$587

million. I had never studied Powerball before, but

quickly put together an analysis after NBC's Today

Show asked me to comment in the segment

they aired the morning of the big drawing.

Powerball had changed their rules less than a year

earlier, raising the ticket price to $2 from $1 and

adjusting the prizes to match. This seemed likely to impact

sales, so I only used data from after the

rule change in my model. Unfortunately, this left me

with only 90 data points, and this model did not perform

as well as the MegaMillions model.

281 million $2 tickets were sold to win the

big jackpot, but the model predicted 54% more: 435

million. I'd predicted a ticket's expected

value for that big drawing

would be 67.3 cents; in reality, it was 83.3 cents --

still well short of its $2 price.

The models weren't perfect, but I think their

fundamentals are sound, and they're much

improved from 2011 now that we have new data points

for huge jackpots.

But, perhaps more importantly, these two tests

demonstrated the most important feature of my analysis.

Before the big 2012 jackpots,

every lottery we'd seen had followed the rule

that a bigger jackpot made for a more valuable ticket.

The idea that superlinear sales would force the value

of a ticket back down again was speculation based

on my model of sales trends.

But we've now seen two jackpots above half a billion

dollars, and my prediction came true:

sales were so strong that the negative effect of ties

overwhelmed the positive effect of having a larger

prize. These two drawings are the first

that are past the peaks seen on the

jackpot-vs.-value graphs --

proving that the peaks exist.

Still, it bears repeating that this analysis rests

on our ability to predict future lottery

sales based on the history of previous sales.

Past $640 million, we have no evidence.

Who knows what will really happen

when a billion-dollar jackpot finally happens?

Maybe with a big enough prize,

the market will saturate --

everyone who knows how to

buy lottery tickets has bought

all the tickets they can afford

and the sales curve gets flat.

For the last word on this topic, however, I

cede the floor to

Durango Bill,

who

aptly observes

that driving to the store to buy a Mega Millions ticket

is more likely to be fatal than it is to make you rich.

That's why I plan to walk.

Jeremy Elson is a computer

science researcher who spends his time outside of work

riding bicycles, flying airplanes, building

electronics, and playing with Mathematica. (This work is a

personal project; I do not speak for my employer.)

Jeremy Elson is a computer

science researcher who spends his time outside of work

riding bicycles, flying airplanes, building

electronics, and playing with Mathematica. (This work is a

personal project; I do not speak for my employer.)